Recursion (RXRX): You really would expect more from a $1.8 billion company

Seems to be a platform drug discovery company where the platform doesn't discovery anything good

First, before diving into today’s topic, I just want to thank everyone who reached out with support following my first post last week. It really made me excited for the future and also provided me with some additional ideas.

One of those ideas is Recursion Pharmaceuticals (RXRX) which has a very Gingko Bioworks-like slogan “decoding biology to radically improve lives”. Essentially, they are another in a long line of companies attempting to take advantage of improved computing power in order to improve drug discovery. In theory, it could work, but as the saying goes, “in theory there is no difference between theory and practice, while in practice there is.”

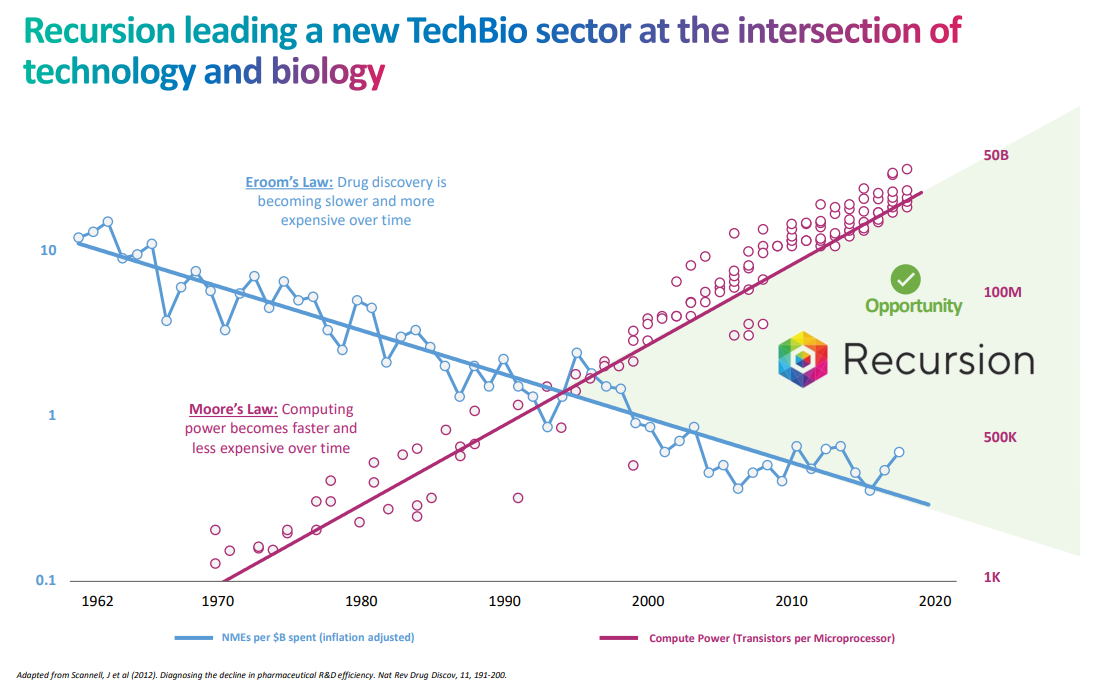

One thing you can certainly tell about the company is they are really trying to get the tech bros into the stock (and probably to get people thinking about network effects and not on the high risk of their clinical programs). How can I tell? First, they refer to themselves as a “TechBio” company instead of biotech. And then they of course have to refer to Moore’s Law in their deck.

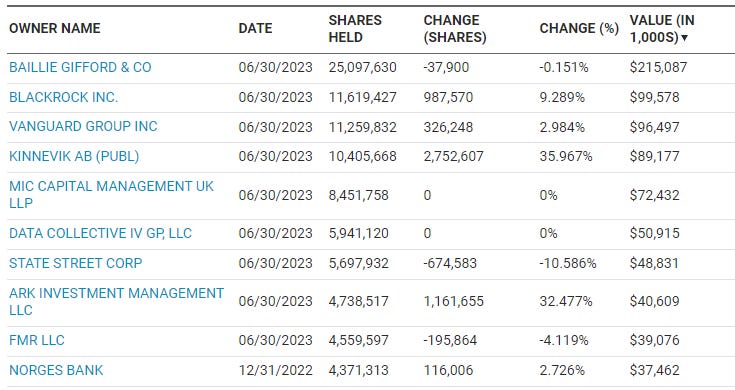

Which I guess was partially successful as they have Cathy Wood’s fund as a top holder. Otherwise it is mainly owned by UK/EU investors and passive funds. One thing you will note is that there aren’t biotech specialist funds in there, which is a bit unusual for a $1.8 billion company claiming to be at the forefront of science. The reason I point this out is simple, these are the funds that actually have people who know what they are doing. Yes, they make mistakes but they usually do deep due diligence before they ever get into a name. Long-only funds, especially European ones, just don’t go that deep, especially not in healthcare. There’s an old joke “why don’t long-only managers look out the window in the morning? Because then what would they do in the afternoon?” That fits them perfectly.

Now let’s look at what they have achieved with their magic black box. Their lead program is REC-994 for Cerebral Cavernous Malformation (CCM). Here is how the company describes it in their 10-K “REC-994 is a small molecule therapeutic designed to alleviate neurological symptoms associated with CCM and potentially reduce the accumulation of new lesions.”

Designed? Really? Contrary to what they might want you to think, REC-994 was not designed to target CCM. It’s a molecule called tempol or 4-hydroxy-2,2,6,6-tetramethylpiperidin-1-oxyl which was first introduced in 1960 that has some industrial uses as a catalyst and chemical oxidant. But you wouldn’t know that from their SEC filings unless you read closely as they mention that REC-994 is tempol exactly once in their 10-K in their section on asset-based collaborations on page 94.

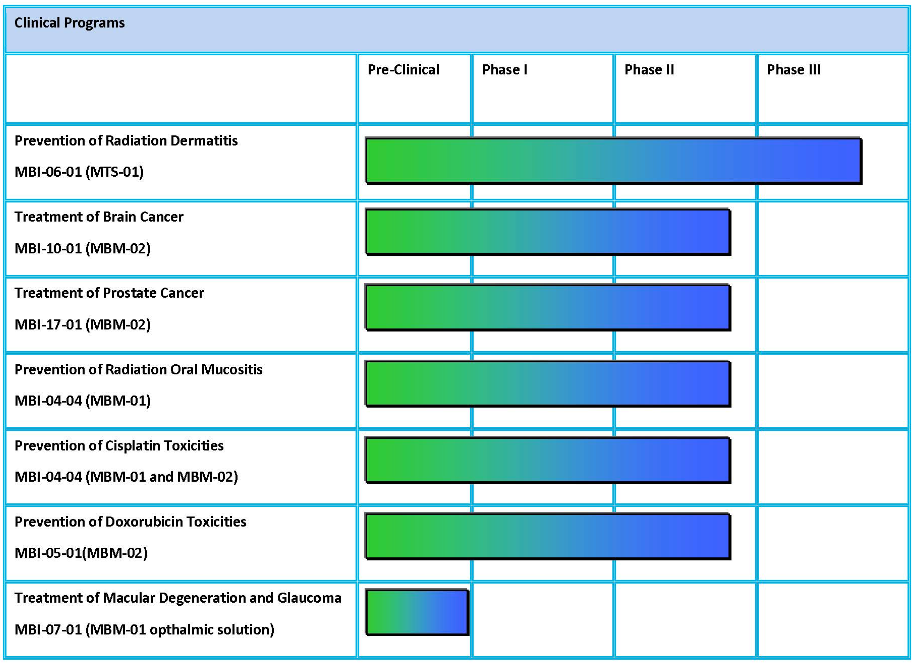

Of course, I can see why they don’t want too much talk of tempol because a simple internet search will bring up a lot of past they might not want mentioned as it would hurt their marketing. Tempol has been tried by at least three other companies recently in a whole host of areas. About 15 years ago it was being developed by Mitos Pharmaceuticals for alopecia related to radiotherapy. More recently, Matrix Biomed took it up and is using it in a variety of cancer-related indications in various forms (see chart below), although as Matrix is a private company it’s unclear what the exact status is currently.

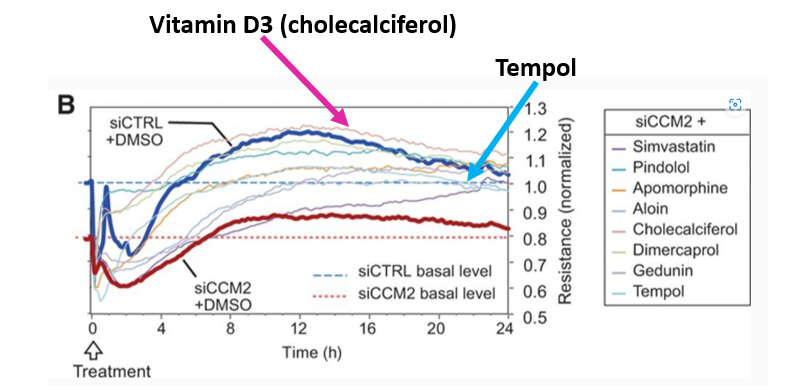

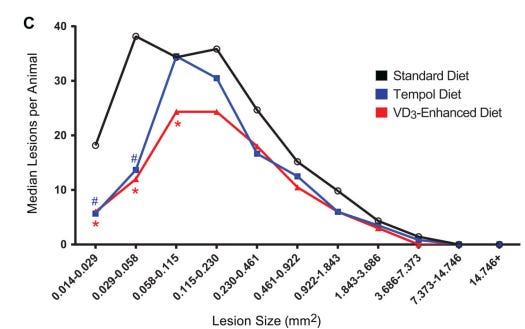

Then of course there was Adamis Pharmaceuticals who enrolled 248 patients in a Phase 2/3 trial of tempol in COVID patients. It failed miserably. I realize that I’m probably being unfair and that the whole Recursion thesis is that their magic box will tell you the right place to go with a compound. Funny thing is, tempol wasn’t even the best molecule to use in CCM based on their own experiments. That molecule is Vitamin D3. Let’s take a look at this publication where the lead author is Recursion co-founder and CEO Chris Gibson (h/t to @jesse_brodkin for tweeting it out). You can see in the chart below, vitamin D3 brought cells closer to normal (which you can define as the thick dark blue line) than tempol.

This finding was confirmed in a mouse study where vitamin d3 supplementation led to fewer lesions.

But anyway, don’t take my word for it, let’s go to the discussion section in that paper written by the co-founder and CEO:

By focusing on such molecules, our high-tech screening method, which combines advances in molecular biology, imaging, and computing, has led to a low-tech solution: the potential for a modulatory role of 2 known drugs on CCM disease. Chief among these is cholecalciferol, which is inexpensive and widely available in supplement form, is freely available outdoors to those with exposed skin, and has a wide safety margin.

So why didn’t they move forward with treating CCM with vitamin D3? Probably because someone informed them there would be no money in it. I can get a year’s supply of 5000IU vitamin D3 for $14 on Amazon. Okay maybe people need a higher dose such as 10000IU per day (which is probably the upper limit of safety for chronic use for most people or even past it), then we’re at $28 for an entire year. And there just wouldn’t be anything they can do to make the vitamin D3 different enough that you would need their proprietary formulation. GW Pharmaceuticals was able to get around the fact that CBD is widely available by the fact that you need a heck of a lot of drug to actually show any efficacy so that getting a prescription and going through insurance would be substantially cheaper than buying it on your own.

And then there is REC-2282, their second most advanced program, for NF2-mutated meningiomas, which I will touch on briefly since the post is already long in the tooth. REC-2282 was previously being developed by the now defunct Arno Therapeutics for a variety of cancers including meningiomas. I wonder where the Recursion magic box comes in with this one because they are just continuing down a road that this molecule was already headed down.

In a pilot study with six patients and 15 evaluable tumors (8 vestibular schwannomas and 7 meningiomas), the drug demonstrated a 0% response rate. The publication claims they had a 7% response rate, but the one they count had 24% tumor shrinkage, which is lower than the usual 30% standard for a partial response. This would be okay in a pilot study if they had room to move up on the dose, but they don’t. There were two dose-limiting toxicities (DLTs) in the 60mg-80mg doses, grade 3 thrombocytopenia and grade 4 psychosis (which I don’t see too often). Hence in the upcoming phase 2 they are only evaluating 40mg and 60mg. So while the study might be interesting from an academic point of view, I wouldn’t bet on any miracles. Cancer, unfortunately, is hard.

Recursion is also developing REC-4881 for familial adenomatous polyposis (FAP) which presents as a large number of precancerous colorectal polyps. REC-4881 was formerly known as TAK-733 when it was being developed by Takeda for oncology indications. In a Phase 1 study which included patients with multiple cancers, out of 41 evaluable patients, they had responses in only 2 of them, both with cutaneous melanoma. REC-3964 is pretty early and is ging after a difficult and crowded indication, C. diff infection. Honestly, you would expect more from a pipeline of a $1.8 billion company.

And then there is the issue of intellectual property. You can see in their 10-K this commentary on the IP of their two most advanced programs:

REC-2282: We exclusively license patents and patent applications related to REC-2282 from OSIF; this patent estate includes composition of matter IP for REC-2282. Our licensed patents related to REC-2282 generally expire between 2027 and 2038, excluding any patent term adjustment or patent term extension.

REC-994: We exclusively license patents in connection with our REC-994 product candidate from UURF; this patent estate is targeted at the use of REC-994 for the treatment of CCM. Our licensed patents related to REC-994 generally expire between 2035 and 2036, excluding any patent term adjustment or patent term extension. Orphan drug exclusivity in the U.S. would run seven years from marketing authorization.

REC-4881: We exclusively license patents and patent applications in connection with our REC-4881 product candidate from Takeda; this patent estate includes composition of matter IP for REC-4881. Our licensed patents related to REC-4881 generally expire between 2027 and 2032, excluding any patent term adjustment or patent term extension. Orphan drug exclusivity in the U.S. for FAP would run seven years from marketing authorization.

REC-3964: This program was generated internally and has pending patent applications that would expire in 2042 excluding any patent term adjustment or patent term extension.

You can see from the description of the REC-994 that they don’t have a composition of matter patent and that the patents they have are related to method of use, which expire in about 13 years. That may seem like a long time, but they are just in a small 62-patient trial which isn’t expected to readout until the second half of 2024. It will probably be 2028 until it even gets on the market, assuming it works. So, the patent life will be a bit more limited than you would like, which is also why they mention the orphan drug exclusivity. REC-2282 has composition of matter but their patent estate as a whole starts to expire in 2027, long before it gets on the market. There’s a similar situation with REC-4881, though that patent estate only extends to 2032. REC-3964 is the only product where they will have a good deal of patent life.

But what about the validation from Nvidia and Roche? Nvidia is not any sort of validation and they have so much money they don’t know what to do with it so why not send it to those who are using AI in exchange for equity? And Roche? I have to admit, it’s a nice deal, we’ll see if anything comes of it. The biggest validation would be that a drug is successfully developed from Recursion’s platform and that will take a long time (and their internal pipeline isn’t likely to have a winner). Just remember, some of these platform collaborations have a big bang but don’t necessarily pan out. Gingko Bioworks has collaborations with companies such as Novo Nordisk, Merck, Solvay and Sumitomo Chemical, what’s that done for them? Let’s look at their stock chart:

Right now, Recursion is riding the AI wave nicely but that won’t last (just like Gingko’s synthetic biology wave). Sure, AI will last but not the urge to buy anything with even a tangential association with it. And they will need to deal with their financing issue. They had $405.9 million in cash as of June 30, 2023, and then got a $50 million infusion from the equity investment from Nvidia. These are cash levels that a lot of biotechs would love to have right now. Unfortunately, they are burning approximately $75 million a quarter (cash flow from operations plus capital expenditures), so they have cash until about the end of 2024, assuming no acceleration. And it really says something when a $50 million infusion only gets you about 2 months’ worth of runway. One last thing on the finances, they are currently guiding for data from REC-994 and REC-2282 in the second half of 2024. These data are very high risk and if they are negative, the stock could easily go into a death spiral ahead of financing. The sellside views the internal pipeline as proof-of-concept for the larger platform, so what happens if the first two readouts fail?

Anyway, we’ll see what happens though I don’t think it’s looking good. I’d probably have a somewhat different view of this company and management if they were more upfront about things, such as the past experiences of the drugs in their pipeline.

Thanks so much for reading! Please like, share and subscribe.

Stocks mentioned: