Greenwich LifeSciences (GLSI): Developing a placebo from a family of placebos

Executive Summary

· Greenwich has one development program, a HER2/neu-based breast cancer vaccine dubbed GP2.

· GP2 is one of three HER2/neu-based breast cancer vaccines developed by George Peoples, a former military surgeon. One went to the infamous Galena (NeuVax or E75), another ended up at Generex (AE37), which went bankrupt, and the third is with Greenwich. All have failed late-stage trials.

· GP2 actually has worse binding to the human leukocyte antigen A2 (HLA-A2) than NeuVax so it’s not even the best candidate in this failed class.

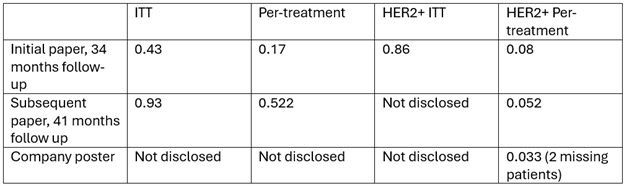

· In a 189-patient Phase 2 study, the initial primary analysis indicated a p-value of p=0.43. That went to p=0.93 after longer follow up.

· Greenwich has focused on the subgroup that had HER2 scores of 3+ and had completed the primary vaccination series to justify moving into Phase 3. In the primary analysis of this subgroup the p-value was p=0.08, p=0.052 in the follow up and then p=0.033 in another follow up that was in a poster that didn’t include any of the original investigators and was missing 2 patients from the initial analyses.

· In February of 2024, the company admitted that one of the patients in the treatment arm, which was not marked as having a recurrence, may have had one. This would have a negative impact on the p-value.

· The company initiated a 598-patient Phase 3 trial in August of 2022 but has not provided any concrete updates on enrollment. Based on the company’s paltry increase in R&D spending from before the trial, it is likely that few patients have actually been enrolled.

Greenwich LifeSciences is one of those companies that when you look at it you are in a bit of disbelief that it is a public company, especially one that has a market cap higher than $5 million (it is around $166 million as I’m writing this). Of course, given the market we’re in, the fact that it has no redeeming value as a company didn’t stop it from rallying about 60% in a little over a week earlier this month.

Greenwich is developing GP2, a HER2/neu-based breast cancer vaccine. GP2 is part of a family of similar peptide-based vaccines coming from George Peoples, a former military surgeon. The three are NeuVax (aka E75), which is derived from the extracellular domain of the HER2 protein, AE37, derived from the intracellular domain and GP2, derived from the transmembrane domain.

NeuVax was taken into Phase 3 by the infamous Galena Biopharma but that trial was stopped in 2016 due to futility in an interim analysis. Galena is infamous because it was implicated in a stock promotion scheme in 2014, which led to the CEO, Mark Ahn, having to resign and of course subsequent securities litigation. Mark Ahn ended up going to prison for insider trading related to another company.

AE37 ended up going to Generex Biotechnology. AE37 was also never able to show any efficacy, failing miserably in a 301-patient trial with a p-value of 0.968. Generex filed for bankruptcy in 2022.

Even among these suboptimal programs, GP2 is actually viewed as a suboptimal target. In one paper it is stated “one concern regarding the use of GP2 in a peptide-based vaccine is that it is a subdominant epitope of HER2, given that it has relatively poor HLAA2 binding affinity when compared to E75.” In other words, it is viewed as inferior to NeuVax! Additionally, in the same paper the authors state that there is a weakness in the entire strategy of using a single peptide vaccine:

The single peptide vaccine strategy may not be optimal, as in both the E75 and GP2 trials, we have found that even though patients are able to expand the number of peptide-specific CTLs in response to vaccination, a large number of patients fail to maintain high levels of immunity without continued antigen exposure.

So of course, it’s of no surprise that just like NeuVax and AE37, GP2 failed as well. In a 180-patient trial the p-value was just p=0.43 in the initial analysis that was published in 2016 which followed the patients for a median of 34 months. In a “per treatment” analysis which excluded 10 patients who didn’t complete the primary vaccination series the p-value was p=0.17. Then they looked at patients with HER2 scores of 3+, indicating HER2+ disease, and the p-value went to 0.86 on an ITT basis. In a per-treatment analysis the p-value was p=0.08. In other words, none of these were statistically significant. And as you can see from the charts below, not terribly compelling.

An update was published in 2020, which had a median of 41 months of follow up. The ITT analysis indicated a p-value of p=0.93, p=0.522 in the per-treatment analysis and a p-value of p=0.052 in the per-treatment analysis of those with HER2 scores of 3+. Once again, still not significant or terribly compelling.

Later in 2020, Greenwich published a poster with 5-year median follow up data. The data is pretty much the same as the previous data in the HER2 3+ pre-treatment group except with longer follow up and now suddenly the p-value is p=0.0338. One suspicious difference is that in the prior papers the GP2 arm had 48 patients and now it has 46. Did those two progress so they were excluded from this poster?

That could explain why none of the investigators involved with the trial were involved with the poster’s authorship, it was just representatives of the company (and the CEO’s daughter).

Another wrench in that poster’s analysis and suddenly significant p-value is this statement from a press release from earlier this month on a potential recurrence in the treatment arm:

As a result of detailed due diligence, the Company became aware in Q4 of 2023 of a potential recurrence in the HER2 positive treated arm. This patient was not reported as a recurrence in the database, on a CRF that should be used for a recurrence, in reports from the lead clinicians to the FDA, or in the 3 or 4 year follow-up data published by the lead clinicians. Some CRFs report a recurrence, but the critical CRF that confirms a recurrence was not completed or entered into the database provided by HJF.

This could easily make the result of even their manufactured subgroup non-significant. As I know I’ve thrown a lot of p-values at you, here is a table summarizing them, including some key numbers that weren’t disclosed:

The company is now in a 598-patient Phase 3 trial that started in August of 2022. Clinicaltrials.gov currently says the estimated date of completion is December 2026 but that is highly unlikely. The endpoints require a median follow up of 4-years and the study is likely barely enrolled. Of course we don’t really know anything about exactly how many patients are in the trial and the company has been hesitant to update investors. See a list of all of the press releases from the company since December 2022:

In all of 2023 they had only one press release and it had nothing to do with the trial (also notice no quarterly earnings releases). The February 2024 press releases say nothing about how many patients are in the Phase 3 but focus on efforts to increase the number of participating centers, especially in Europe.

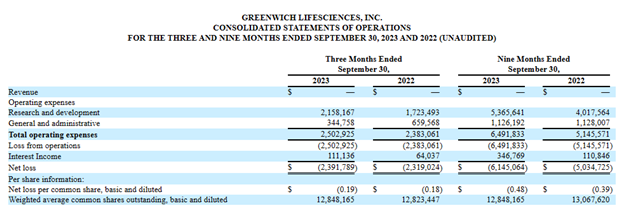

Based on their 10-Q for the period ending September 30, 2023, it doesn’t appear that they can be enrolling many patients. All R&D expenses for the quarter were $2.2 million, a paltry amount for a company supposedly running a large Phase 3 trial. And the total was just a little over $400,000 higher than what was spent in the same quarter a year ago, which did not include a single patient (first patient enrolled was in December 2022). Considering companies are often spending $100,000 per patient or more for clinical trials, this indicates an extremely small number of enrolled patients.

It’s not inconceivable that this trial won’t actually complete until 2029 or later (if ever). One other point, usually enrollment rates correlate quite strongly with investigator and patient excitement for the therapy, clearly there just isn’t any.

This is one of those rabbit hole companies where there is just an infinite amount of information that I could convey but as you can see, I’ve already shown they have a zero chance of success in any large trial given both the prior data as well as the performance of related compounds. So I’ll be brief and just mention that the company appears to have optioned a program from its own CEO (note the line in the press release “The founder of Westport Bio is Snehal Patel, CEO of Greenwich LifeSciences”, h/t White Diamond Research). That they recently fired one no-name auditing firm and replaced it with another. That the CEO owns 42% of the company and hence is likely not accountable to anyone. That the CMO appears not to be full time despite Greenwich sponsoring a large trial as he is currently an executive at 2 nutraceutical companies. That both the Chairman of the Board and head of regulatory were involved with the disasters that were Repros and Opexa. That the company only had $9.1 million in cash as of the end of September of 2023 and so would need a large capital infusion to complete the trial (I estimate the trial by itself would cost around $60 million). And this is not even an exhaustive list (not even close).

This company has more red flags than a May Day parade.

Please like, share and subscribe!

Disclaimer: I do not hold a financial position in Greenwich LifeSciences (GLSI) nor do I have any financial incentive for the stock to move in any direction or for it to become more volatile. This post is purely for informational purposes only and is not meant as financial advice nor as an encouragement to trade. I definitely suggest you do your own research and/or have a discussion with a financial advisor.

Stocks mentioned: