Altimmune (ALT): Odd drug out

Weight loss by itself isn’t enough

You have to hand it to the Altimmune management, they really know how to catch the latest wave. Today it is obesity, but a few years ago it was COVID. Back in 2000, they were able to start the year at $1.89 per share and reach a peak of $28.18 in August because of their intranasal COVID vaccine candidate dubbed AdCOVID. In December of that year, the FDA placed a clinical hold on the program due to CMC issues and then in July 2021, the company scrapped it.

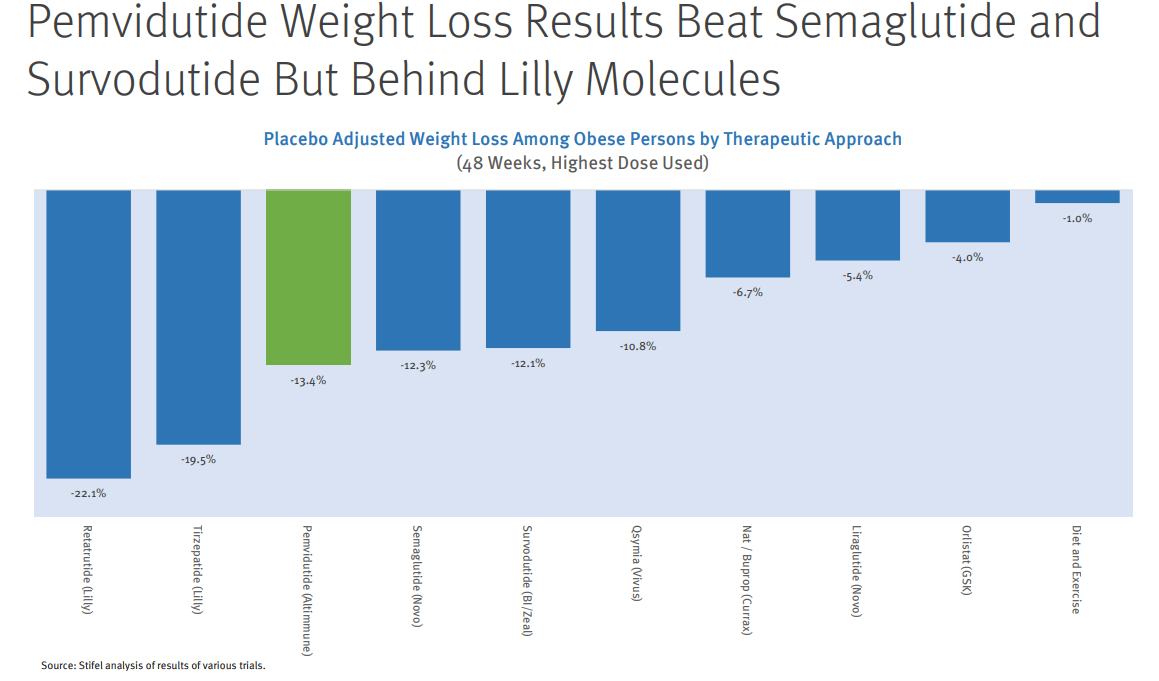

Back to obesity, the stock has received a boost recently because of their Phase 2 data in obesity for pemvidutide, an injectable dual GLP-1/glucagon receptor agonist. Granted, the actual weight loss data was pretty decent, though was behind Lilly’s Mounjaro (tirzepatide), which targets GLP-1/GIP and Lilly’s retatrutide, which targets GLP-1, glucagon and GIP together, and recently had blockbuster Phase 2 data (chart per Stifel).

Several years ago, this result would have been grounds for Altimmune to have a multi-billion dollar valuation, today is a bit different thanks to the intense level of competition in obesity (chart per Evercore ISI, highlighted programs are ones which include GLP-1 + glucagon).

Boehringer Ingelheim has a program, survodutide, with the same exact mechanism as pemvidutide, which showed a very similar degree of weight loss and adverse events. Mazdutide from Innovent/Lilly showed slightly better weight loss and far fewer discontinuations but that was a Chinese trial so it’s not an apples-to-apples comparison.

But then more important is the competition from players that don’t use glucagon agonism as part of their mechanism of action. If you look at the table below from the Mounjaro review documents, you’ll see that while patients receiving placebo had a slight increase in their fasting plasma glucose, those on Mounjaro (and those on semaglutide in the trial where it was the control) had a marked decrease in that very key statistic.

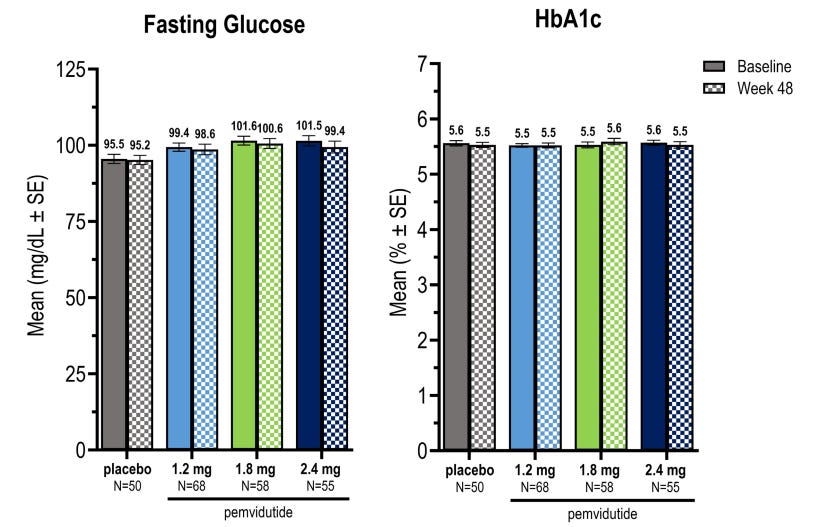

Now let’s look at what happened in the Altimmune trial:

Despite the fact that people lost 32 pounds on average in the high dose pemvidutide arm, their fasting blood glucose (as well as their HbA1c) barely budged. Does that sound right to you? Isn’t part of the reason people want to lose weight is to improve glycemic control?

On the conference call, the company argued “these were normal glycemic subjects and we would not expect to see any material reductions from baseline in these patients.” True, you wouldn’t see the 40-60 point reductions like with Mounjaro but how about 5-10? A fasting plasma glucose of 100mg/dl is not exactly ideal and in fact is borderline pre-diabetic per the ADA.

Considering 38% of all US adults (whether obese or not) are prediabetic, this all seems very important for the ultimate commercial potential for the product. And just on a personal note for some perspective, I was diagnosed with prediabetes several years ago. I have been successfully able to manage that through diet and exercise. But if after all that work, my fasting plasma glucose didn’t budge, I’d be very frustrated, so don’t underestimate how negative this profile is for this drug.

And the competition from those without glucagon agonism as part of the mechanism is only going to get worse. Roche recently purchased Carmot for $2.7 billion. Carmot is developing CT-388, a GLP-1/GIP receptor agonist. What makes this one really special is the 7.6% placebo-adjusted weight loss seen at just 4 weeks in their 64-patient Phase 1/2 trial. Amgen’s AMG133 was even higher though as that was in just 6 patients, a lot remains to be seen from that one (chart per Stifel).

The drugs I have mentioned so far, including Altimmune’s, were injectable but there are oral drugs in development which will likely take the vast majority of the market if approved (people always prefer convenience and a lack of needles, even if they are very small). Lilly’s orfoglipron is an oral GLP-1 receptor agonist, which showed a 12.4% placebo-adjusted weight loss at 36 weeks, essentially in-line with Altimmune, in a 272-participant trial. Additionally, HbA1c, a measure of glycemic control, went from borderline prediabetic to more normal levels (as a reminder, essentially no change was seen on this measure in a similar population with Altimmune’s drug).

Structure Therapeutics also recently released data on their oral GLP-1 from their 94-participant Phase 2a trial, demonstrating 4.7% placebo-adjusted weight loss at 8 weeks in the obesity cohort of the trial. They also saw statistically significant reductions in fasting plasma glucose and HbA1c. Importantly, there was only 1 discontinuation due to an adverse event from the study drug in the 60 patients who received GSBR-1290. That amounts to just 1.7%. As a comparison, Altimmune saw an order of magnitude greater discontinuation rate in their trial (around 16% in each of the two highest dose arms).

All that to say that I think Altimmune’s pemvidutide is going to be the odd man out in what looks to be a very crowded, consumer-oriented space. There just aren’t any positive differentiating factors and at least one key negative one, the lack of improvement in glycemic control. It’s going to be a tough sell both to consumers and to pharma partners. Just remember that obesity trials will need to be enormous. Mounjaro was tested in over 6,000 patients! Based on numbers like that, a potential partner would need to invest over $1 billion just on the Phase 3 program. Then let’s not forget manufacturing, direct-to-consumer advertising and a large salesforce. All while navigating the inevitable political backlash over the cost of these drugs (not something to ignore after they passed the “Inflation Reduction Act” and are even talking about march-in-rights on patents!). They’d have to be a big believer and I just don’t see how that happens with this drug.

I might feel differently if they had a management team that has successfully navigated such challenges before. But it’s actually the exact opposite. Even before their COVID vaccine debacle, both the CEO and CFO had the same positions at Neos Therapeutics (which had the ticker “ADHD”). Neos was developing/commercializing reformulated ADHD meds such as a melt-in-your-mouth Adderall.

In October 2017, they received a bid from PDL BioPharma for $10.25 per share, one which they turned down despite being at a 40% premium. By June of 2018, Neos was 40% lower than the bid price and CEO Vipin Garg abruptly resigned. By the end of 2018, the stock was at $1.65, down 84%. It certainly didn’t help that the CEO had left the company’s financials in shambles. As of June 30, 2018, the company had $28 million in cash, $34 million in accrued expenses, $16 million in the current portion of long term debt, and another $44 million in non-current long term debt. All this while burning around $10 million a quarter.

Before that, the CEO and CFO were at Tranzyme together. That didn’t end well either. See the below from a Genetic Engineering and Biotechnology News story from 2013:

The statement came less than two years after Tranzyme went public, and less than two months after the company pulled the plug on a Phase IIb study on the effects of three-times-daily dosing of its lead drug candidate, TZP-102 in patients with diabetes who have gastroparesis. The company was looking for signs of improvement over the 12-week treatment period in upper GI symptoms associated with the disease, such as nausea, vomiting, dehydration and difficulty digesting food.

“The results are consistent with the findings of a prior Phase IIb trial in that there was a very large placebo effect and no treatment effect,” Transzyme said in a December 17, 2012, statement following the end of the latter trial, which assessed once-daily dosing.

Earlier last year, Tranzyme suffered a double setback when its gastrointestinal drug candidate ulimorelin, co-developed with Dutch-owned Norgine, failed not one, but two Phase III trials. In one trial, ULISES 007, ulimorelin failed its primary endpoint of statistical improvement vs. placebo for GI2—time to recovery of GI function from the end of surgery to either first bowel movement or tolerance of solid food, whichever was later. In the second trial, ULISES 008, the drug failed to meet endpoints for accelerating GI recovery in patients who had undergone partial bowel resection.

At this point, I won’t even go into the fact that the CMO was involved with Napo Pharmaceuticals/Jaguar Health and the infamous Lisa Conte.

That said, unlike a lot of the other companies that I’ve written on, there is something here. They have data exactly as you would expect from a GLP-1/glucagon agonist. My point though is that given the incredibly crowded landscape filled with drugs that are superior in one way or another, I don’t see a place for Altimmune’s pemvidutide. And given the history of the management, they really don’t seem like the type to beat the odds.

Please like, share and subscribe!

Stocks mentioned: